The Kingdom of Cash is not an African Country.

Cash is and will remain relevant in the African ecosystem for a long time yet to come. Disappearing cash transactions in the rest of the world and even cashless economies worldwide will not see cash disappear completely. In the African context, it will take a lot longer. Read more

Ysaac Akinin

3/31/20252 min read

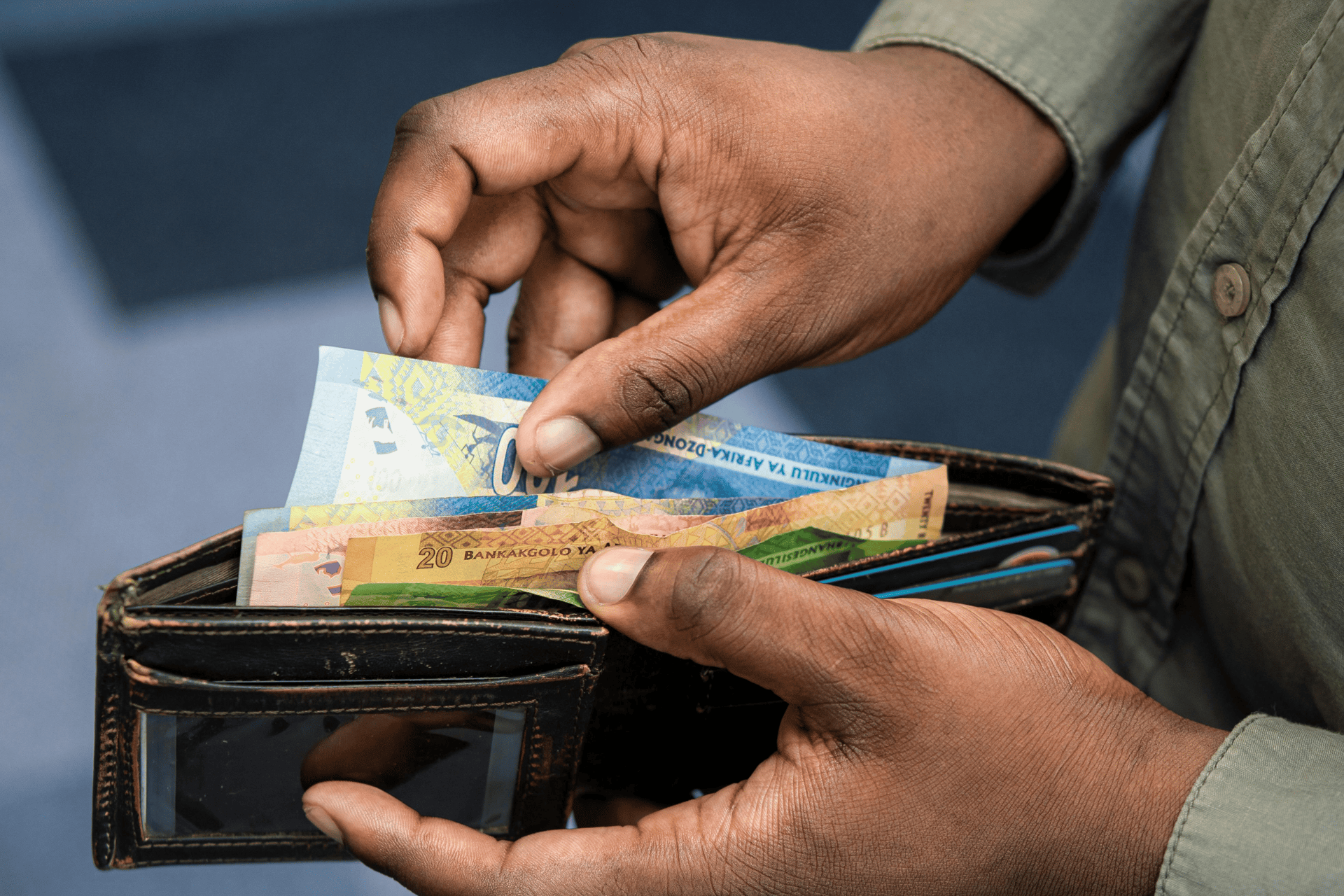

While the global push toward cashless economies accelerates, in Africa, the notion that cash is nearing obsolescence remains disconnected from reality. Nearly 80% of business transactions on the continent still take place in cash—evidence not of backwardness, but of pragmatism. Cash endures because it continues to align with Africa’s infrastructural, cultural, and economic landscape in ways digital finance cannot yet match.

Digital financial services are expanding, and mobile money has achieved undeniable success in places like Kenya and Ghana. However, financial inclusion remains uneven. Millions across rural and low-income communities lack smartphones, internet access, digital literacy, or even basic identification documents. In such contexts, cash is not simply preferred—it is indispensable. It functions without power, passwords, or a data plan. It is universal, instant, and offline.

Even in more connected areas, the reliability of digital infrastructure is inconsistent. Power outages, weak network coverage, high mobile fees, and lack of point-of-sale systems prevent seamless digital transactions. For informal vendors, transport operators, and street markets—the lifeblood of Africa’s economies—cash is not just more convenient; it is often the only viable means of conducting business.

Trust, too, plays a pivotal role. Many Africans remain skeptical of banks and fintech platforms due to past experiences of service failure, hidden fees, cyber fraud, or institutional instability. Cash, by contrast, is tangible and transparent. It offers control and certainty—qualities that are hard to replace with pixels and passwords. In many households, especially among women and older generations, cash also provides discretion in managing funds away from unwanted scrutiny.

This connects to deeper social and cultural dynamics. In many communities, cash supports informal savings groups, gift-giving, tithing, and family remittances. More delicately, it enables secrecy in handling family funds—sometimes as a protective strategy—and serves as a shield against overreach by spouses, relatives, or even the state. Tax avoidance, though rarely discussed openly, is also entwined with cash preference. In economies dominated by informal work, many resist digital transactions precisely because they increase traceability and potential taxation in systems often perceived as inefficient, punitive, or corrupt.

The future of finance in Africa is undeniably digital—but not exclusively so. Pushing for total digitization without addressing the underlying barriers risks widening the gap between formal and informal economies. A hybrid approach that integrates cash into the digital ecosystem, through cash-in/cash-out agents, smart safes, and interoperable platforms, offers a more realistic and inclusive path.

Cash in Africa is not a failure of innovation—it is a reflection of resilience, mistrust, and adaptation to real constraints. Its endurance is not in spite of Africa’s progress, but because of the complex, unvarnished truths about how most Africans live, earn, and transact. Until digital systems can rival cash in reach, reliability, and cultural fit, cash will remain not just relevant—but vital.

Empowering Africa's cash

Summit

Connecting Africa's cash ecosystems

Innovation

Empowerment

info@africashsummit.com

+260 97 9173179

© 2025. All rights reserved.